The 2026 Reality Check: Why the Government Won't Save Your Family If the Worst Happens

We all know the script: grow up, get a good job, buy a house, have kids, and assume everything will work out. We pay our taxes and mandatory Canada Pension Plan (CPP) deductions every paycheck, operating under the quiet assumption that the social safety net will catch our families if tragedy strikes. As of February 2026, that assumption is mathematically dangerous. To understand the massive gap between statutory payouts and the brutal reality of the Canadian economy, let’s look at a real-world scenario.

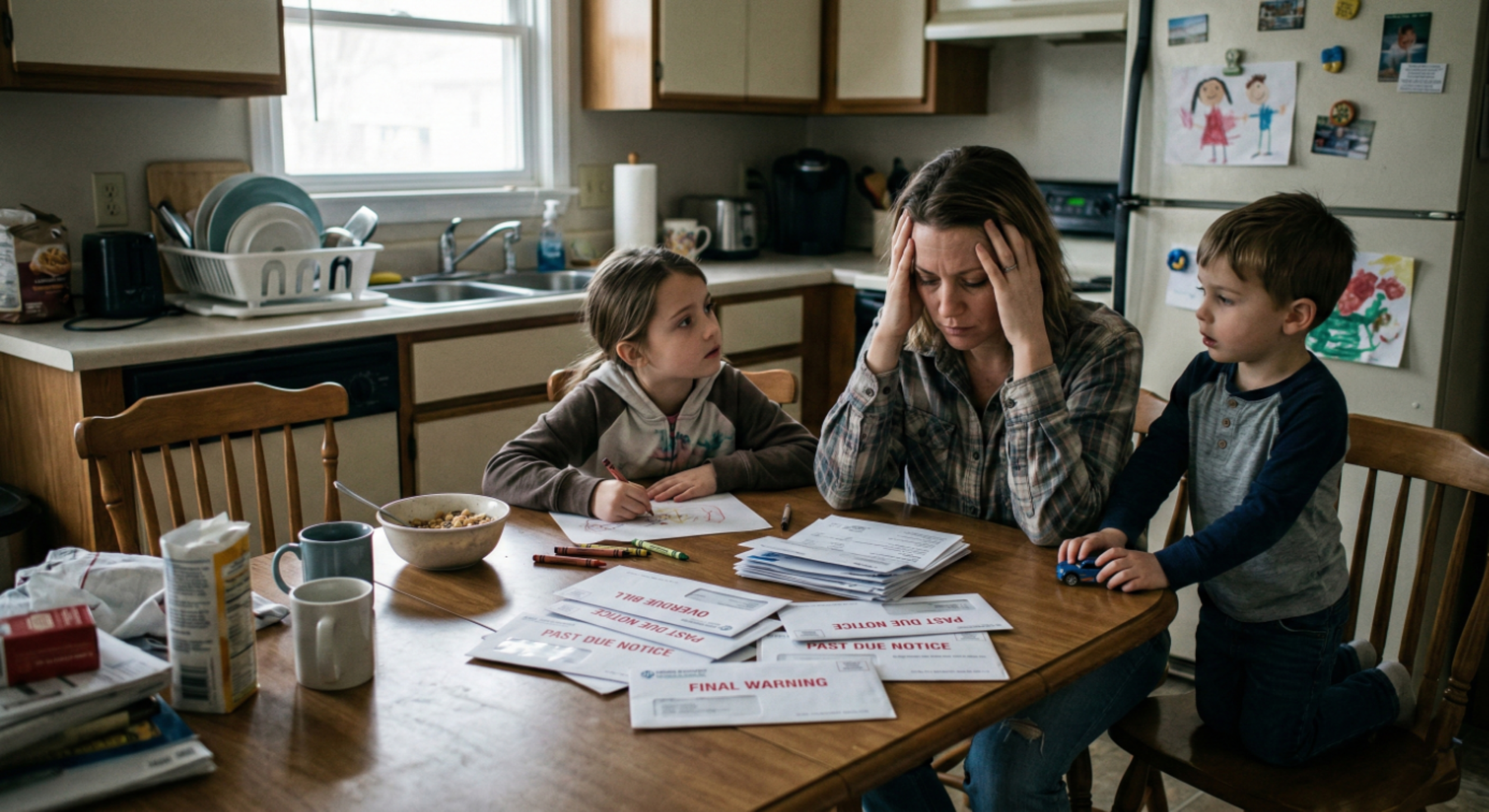

Meet Sarah, a 38-year-old living in the Greater Toronto Area with her husband, Mark, and their two young children, Leo and Mia. Between Sarah’s $65,000 salary and Mark’s income, they comfortably navigate their mortgage, car loans, and childcare costs. But in February 2026, Mark dies unexpectedly. Like 42% of Canadians, Mark had no private life insurance, assuming his CPP contributions and home equity were a sufficient backup plan. Within days, Sarah's financial reality shatters. Her first shock arrives at the funeral home, where a standard Toronto funeral frequently exceeds $10,000. Sarah expects the highly publicized 2025 CPP $5,000 death benefit "top-up" to cover the costs, but she quickly discovers a cruel legislative catch. The extra $2,500 is only available if the deceased leaves behind no eligible surviving spouse or dependent children. Because Mark left behind a family, Sarah is locked out of the top-up, receiving only the taxable base maximum of $2,500. She is instantly forced to put the $7,500 deficit on a high-interest credit card.

The financial bleeding accelerates when Sarah calculates her new monthly income. While the 2026 theoretical maximum CPP survivor’s pension is $803.54, payouts are heavily diluted by lifetime contribution averages. Sarah receives the national average for new beneficiaries: just $533.55 per month, plus an orphan’s benefit averaging $301.77 per child. In total, the government provides $1,137.09 a month to replace Mark's entire salary. This fraction of income instantly collides with the 2026 cost of living. A standard two-bedroom accommodation in the Toronto area averages around $1,958 a month, and despite political promises, infant childcare still hovers around $22 a day in many Ontario cities. Furthermore, Sarah is now solely responsible for servicing their share of the $541,851 in total debt carried by the average Canadian household in their age bracket, all while facing the $293,000 statistical cost of raising each child to adulthood.

Within three months, Sarah is drowning in debt. This is the exact moment where private life insurance is designed to step in. A tax-free lump sum of $750,000 would have cleared the family's debt, funded the children's education, and replaced Mark’s lost income. Instead, Sarah's tragedy highlights a terrifying national crisis: even insured Ontario households face a 30.5% under-insurance gap, holding an average of $552,000 when $794,400 is required for solvency. The math of 2026 is unforgiving. The CPP is a pillar for poverty alleviation, not income replacement. Relying on a $2,500 death benefit to pay for a $10,000 funeral, or a $533 monthly pension to pay a $2,000 mortgage, guarantees generational financial ruin. Private, adequately capitalized life insurance is no longer a luxury—it is the only reliable bridge across the modern Canadian cost of living.